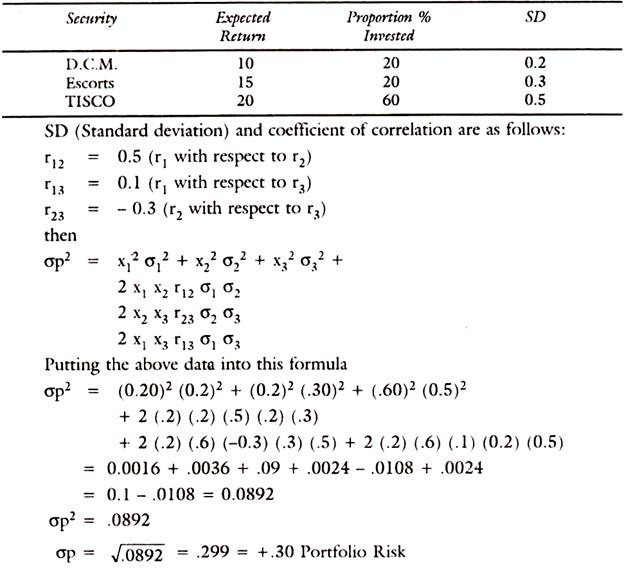

standard deviation of portfolio

|

Econ 422 Summer 2006 Final Exam Solutions

Using the information in the diagram sketch the portfolio expected return and standard deviation values for portfolios of T-bills and Boeing stock for values. |

|

SAMPLE MID-TERM QUESTIONS William L. Silber HOW TO

In a portfolio where you own positive amounts of two risky assets the standard deviation of the portfolio cannot be reduced below the standard deviation of |

|

Outline Portfolio Expected Return and Standard Deviation

Optimal portfolio choice with 2 risky assets With 2 securities the portfolio variance is: ... 'volatility' is another word for 'standard deviation'. |

|

Chapter 1 Portfolio Theory with Matrix Algebra

Aug 7 2013 and portfolio standard deviation |

|

Naive Diversification and Portfolio Risk-A Note

It is then shown that past empirical studies which have used this methodology are deficient. (PORTFOLIO; STANDARD DEVIATION; VARIANCE; NAIVE DIVERSIFICATION). |

|

Safety-First and Expected Utility Maximization in Mean-Standard

mean-standard deviation portfolio analysis the in which the investor compares portfolios on the basis of. |

|

Number of Stocks in Portfolio and Risk Reduction

Risk could be measured by the standard deviation of portfolio return and it in- cludes two elements: systematic risk and unsystematic risk. |

|

STANDARD DEVIATION AND PORTFOLIO RISK JARGON AND

One that arises in the investment side of actuarial science is "risk". There is a widespread use of the standard deviation of periodic returns as a measure of |

|

Pedagogical Note: The Correlation of the Risk- Free Asset and the

two-asset portfolio is a linear combination of the assets' expected returns. of expected return and standard deviation (or variance) would prefer ... |

|

COMM308 MT2 Practice Problems (F21)

standard deviation of Apple Inc. stocks' returns is 10%. What fraction of your wealth should be invested in the risk-free asset so that your portfolio will. |

|

3 Basics of Portfolio Theory

Although it is quite difficult to quantify risk one useful measure of risk is the standard deviation of the returns designated by ? 3 3 Portfolio |

|

Chapter 7 Portfolio Theory - http:/ /wwwitscaltechedu

What are the variance and StD of a portfolio with 1/3 invested The volatility (StD) of portfolio return is: Standard Deviation ( per month) |

|

STANDARD DEVIATION AND PORTFOLIO RISK JARGON AND

"Risk" in this graph is measured by the standard deviation of total monthly returns while the Return is just the annualized total return over the period |

|

Portfolio risk

The risk of a portfolio is measured by the variance (or standard deviation) of its return Although the expected return on a portfolio is the weighted average |

|

Outline Portfolio Expected Return and Standard Deviation - NYU Stern

The minimum variance portfolio (mvp) is the portfolios that provides the lowest variance (standard deviation) among all possible portfolios of risky assets |

|

Chapter 8

two stocks that have a correlation coefficient of 75 Portfolio Weight Expected Return Standard Deviation Apple 50 |

|

Portfolio Theory & Financial Analyses: Exercises - WBI Library

- Risk is measured by the standard deviation of returns and the overall expected return measured by a weighted probabilistic average Page 12 Download free |

|

Risk and Return – Part 2

2 Looking forward Ex ante expectation standard deviation correlation coefficient and covariance of returns 3 Portfolios Portfolio weights |

|

Portfolio Standard Deviation (Formula Examples) - WallStreetMojo

A Portfolio with a low Standard Deviation implies less volatility and more stability in the returns of a portfolio and is a very useful financial metric when |

How do you find the standard deviation of a portfolio?

In order to calculate standard deviation, figure out the mean or the average in the data set. For each of those numbers and square the result. Once that's done, determine the mean of each of those squared differences, then take the square root of that figure. The result is the standard deviation.What is portfolio standard deviation (%)?

Portfolio Standard Deviation is the standard deviation of the rate of return on an investment portfolio and is used to measure the inherent volatility of an investment. It measures the investment's risk and helps analyze a portfolio's stability of returns.- Say there's a dataset for a range of weights from a sample of a population. Using the numbers listed in column A, the formula will look like this when applied: =STDEV. S(A2:A10). In return, Excel will provide the standard deviation of the applied data, as well as the average.

|

Risk and Return – Part 2

Ex ante expectation, standard deviation, correlation coefficient, and covariance of returns 3 Portfolios Portfolio weights Short selling Expected returns |

|

3 Basics of Portfolio Theory

Although it is quite difficult to quantify risk, one useful measure of risk is the standard deviation of the returns, designated by σ 3 3 Portfolio Formation A portfolio |

|

Chapter 7 Portfolio Theory

Consider again investing in IBM and Merck stocks Mean returns ¯r 1 ¯r 2 0 0149 0 0100 Covariance matrix |

|

Standard Deviation and Portfolio Risk - Simon Fraser University

STANDARD DEVIATION AND PORTFOLIO RISK JARGON AND PRACTICE K L Weldon Department of Statistics and Actuarial Science Simon Fraser |

|

Outline Portfolio Expected Return and Standard Deviation - NYU Stern

Portfolio: expected return and SD Diversification Optimal portfolio choice with 2 risky assets Prof 'volatility' is another word for 'standard deviation' Prof |

|

Chapter 11 Expected Returns Variance and Standard Deviation

Deviation • Variance and standard deviation still measure the volatility of returns Portfolios • A portfolio is a collection of assets • An asset's risk and return is |

|

Getting More Out of Two Asset Portfolios - CORE

the Efficient Frontier for a Portfolio of Two Risky Stocks The equations for calculating a two-asset portfolio's mean and standard deviation are available in any |

|

The Magic of Diversification - White Oaks Wealth Advisors

Any level of diversification will reduce portfolio standard deviation and will mean the portfolio's risk-adjusted return will be better than the weighted average risk- |

|

Portfolio Risk and Return - James Madison University - (educjmu

Consider the following investments and the associated expected return and risk ( measured by standard deviation): In portfolio theory, we assume that investors |

PFE Chapter 12: Portfolio statistics CHAPTER 12: STATISTICS")

INVESTMENT MANAGEMENT (FINC 702) LECTURE 6 Practice Questions")